One of the questions I am asked most often by clients who are building international businesses, accumulating assets across borders, or planning for the next generation is this: should I have a trust, a foundation, or just a company? The question sounds simple. The answer is anything but. These three structures are used for broadly similar goals, they can sometimes substitute for each other, and they are often combined in the same overall architecture. But the way they work, the legal nature they carry, the control they permit, and the protection they provide are fundamentally different. Choosing the wrong one does not just cost money to unwind. It can leave assets exposed in ways that only become visible at the worst possible moment.

I have spent decades structuring international holding arrangements across the UAE, Nevis, Seychelles, and a range of European and Asian jurisdictions. In that time the number of clients who arrive with the wrong structure in place, or no structure at all, has never fallen. This guide is my attempt to give you a clear, practical framework for understanding the differences before you sit down with an advisor, so that the conversation you have is a productive one rather than an expensive education from scratch.

- The Three Structures at a Glance

- What a Trust Is and How It Actually Works

- What a Foundation Is and Why It Is Different

- Why European Foundations (Stiftungen) Fail for Asset Protection — The Benko Case

- What a Holding Company Does and Where It Falls Short

- Side by Side: The Full Comparison

- Asset Protection Against Creditors — Which Wins

- Control: The Most Misunderstood Trade-Off

- Civil Law vs Common Law — Why Jurisdiction Matters More Than You Think

- The UAE Context: DIFC, ADGM and Offshore Options

- When You Need All Three — The Layered Structure

- Frequently Asked Questions

The Three Structures at a Glance

Before going into detail on each, it is worth establishing the conceptual difference that underlies all three, because without that the specific comparisons will not make complete sense.

A Trust is not a legal entity. It is a legal relationship. When you create a trust, you transfer your assets to a trustee who holds them for the benefit of named or described beneficiaries. Legal ownership of the assets belongs to the trustee. Beneficial ownership belongs to the beneficiaries. You, as the person who created the arrangement, are called the settlor or grantor. Once you have transferred assets into a properly structured irrevocable trust, those assets are no longer legally yours.

A Foundation is a legal entity. It owns its own assets. It is formed by a founder who transfers assets to the foundation, after which those assets belong to the foundation itself. Not to the founder, not to trustees, not to beneficiaries in any direct sense. The foundation is governed by a charter and regulations, administered by a council, and may appoint a protector to oversee the council's actions. The core distinction is straightforward: a trust is a relationship; a foundation is an entity.

A Holding Company is a corporate vehicle incorporated under company law. It can hold shares in other companies, investments, real estate, intellectual property, and any other asset class. The shareholder owns the company. The company owns the assets. The shareholder's ownership of the company remains part of their personal estate unless that ownership is itself held inside a trust or foundation above it in the structure.

What a Trust Is and How It Actually Works

A trust deed is the founding document of any trust arrangement. It defines the powers of the trustee, the rights (if any) of the beneficiaries, and the settlor's letter of wishes. Getting the drafting right at the outset is not optional.

The origins of the trust lie in English common law, developed centuries ago to allow landowners to transfer property to a trusted person who would manage it for the benefit of their family. The basic mechanics have not changed: a settlor transfers assets to a trustee, the trustee manages those assets according to the trust deed, and the beneficiaries receive distributions or benefits over time. A trust is created when a settlor transfers assets to a trustee, who then manages those assets for beneficiaries. The trustee becomes the legal owner, while the beneficiaries hold equitable rights. This split between ownership and benefit is what gives trusts their power: it enables flexible distribution, strong asset protection, and planning that adjusts as life circumstances change.

The key variable within trusts is whether they are revocable or irrevocable. A revocable trust means you can change its terms or terminate it at any time. That also means it provides almost no asset protection, because in the eyes of the law you effectively still control the assets. An irrevocable trust, by contrast, removes your ability to take back control once assets have been transferred. That is what creates the protection. Courts cannot easily reach assets that you do not own. Creditors cannot claim against assets that no longer form part of your estate. The price of that protection is genuine loss of control, and many clients find that trade-off uncomfortable until they understand what they are actually buying with it.

The other major variable is whether the trust is discretionary or fixed interest. In a discretionary trust the trustee decides which beneficiaries receive distributions, in what amounts, and at what times. This is a powerful feature for creditor protection because no beneficiary has a legally enforceable entitlement to any specific distribution. A creditor cannot seize something the beneficiary has no guaranteed right to receive. A fixed interest trust grants beneficiaries defined rights to specific distributions, which is simpler to administer but provides weaker creditor protection because those entitlements can in principle be reached.

Strong offshore trust jurisdictions for asset protection purposes include St. Kitts and Nevis, whose trust legislation dating from 1994 provides some of the most robust creditor protection provisions in the world, the Cook Islands, the Cayman Islands, and the British Virgin Islands. Within the UAE, DIFC trust law provides an internationally recognised common law framework that is particularly well-suited to families with assets in the Gulf region and beyond.

What a Foundation Is and Why It Is Different

A foundation's charter is typically a public document, while the regulations that govern distributions and the founder's intentions remain private. This combination of transparency and privacy is one of the foundation's distinctive features.

The foundation as a legal concept originated in civil law jurisdictions, particularly in Liechtenstein, where the Liechtensteinische Anstalt (establishment) and Stiftung (foundation) were developed as vehicles for private wealth management. Panama adopted foundation legislation in 1995. Seychelles and Nevis followed. The DIFC and ADGM within the UAE both have dedicated foundation regulations that have been well-tested since their introduction and are now widely used by international families.

A foundation is a legal entity that holds and manages assets in accordance with its charter and regulations. Unlike a trust, a foundation has its own separate legal personality and can own assets in its own name. The founder, comparable to a settlor in a trust, is the individual who donates assets to the foundation. Once transferred, these assets no longer form part of the founder's personal estate and become the property of the foundation.

The governance of a foundation consists of several defined roles. The founder establishes the foundation and transfers assets to it. The council (comparable to a board of directors or to trustees) manages the foundation's assets and operations according to the charter. Beneficiaries are individuals or entities designated to receive benefits, but they hold no ownership rights over the foundation's assets. A protector may be appointed to supervise the council and ensure the founder's intentions are respected over time. A foundation is governed by two main documents. The foundation charter is usually a public document available for inspection. The foundation regulations remain private and can outline the founder's intentions and the mechanisms for distributing assets.

The practical advantages of the foundation over a trust begin with recognition. Select a trust for legal certainty in common law jurisdictions like the UK, but opt for a foundation if operating in civil law countries where corporate-style entities are more readily recognised for business and banking. Foundations can open bank accounts, hold shares directly, enter contracts, and engage with counterparties in their own name. This makes them considerably simpler to work with operationally than a trust, where the trustee as an individual or corporate entity is the counterparty in every transaction.

For the foundation and trust services we provide through 1Stop Connect, the Nevis and Seychelles frameworks are our most commonly used, because they combine strong asset protection legislation with cost-effective administration and excellent international recognition. The DIFC Foundation Regulations are our recommendation for clients who want a UAE-based structure with the highest level of international recognition and a court system that can enforce their governance documents.

Why European Foundations (Stiftungen) Fail for Asset Protection — The Benko Case

The unfinished Elbtower in Hamburg became a symbol of the Signa Group's collapse — and of what happens when a private foundation structure built under European law meets a determined insolvency administrator and a court with reach.

No recent case illustrates the difference between a European foundation and an offshore foundation more vividly than the collapse of René Benko and his Signa empire. Benko was for two decades one of the most celebrated entrepreneurs in the German-speaking world. At his peak he owned the Chrysler Building in New York, the Selfridges department stores in the UK, Karstadt and Kaufhof in Germany, the Goldenes Quartier in Vienna, an unfinished skyscraper in Hamburg, and a real estate portfolio that spanned across Europe and into Manhattan. He was named Man of the Year by the Austrian business magazine Trend. He ran his empire through Signa Holding, a group with a self-declared portfolio of €27bn and development projects worth €25bn. He parked his private wealth in a web of private foundations, the Stiftungen, with the apparent goal of separating his personal assets from his business liabilities. When everything collapsed, the foundations collapsed with him. The case is now one of the most studied examples of why European foundations, despite their respectable legal framework, are often poor vehicles for genuine asset protection.

Understanding what went wrong requires understanding both what Benko built and why the law reached in and took it apart.

The Structure Benko Built

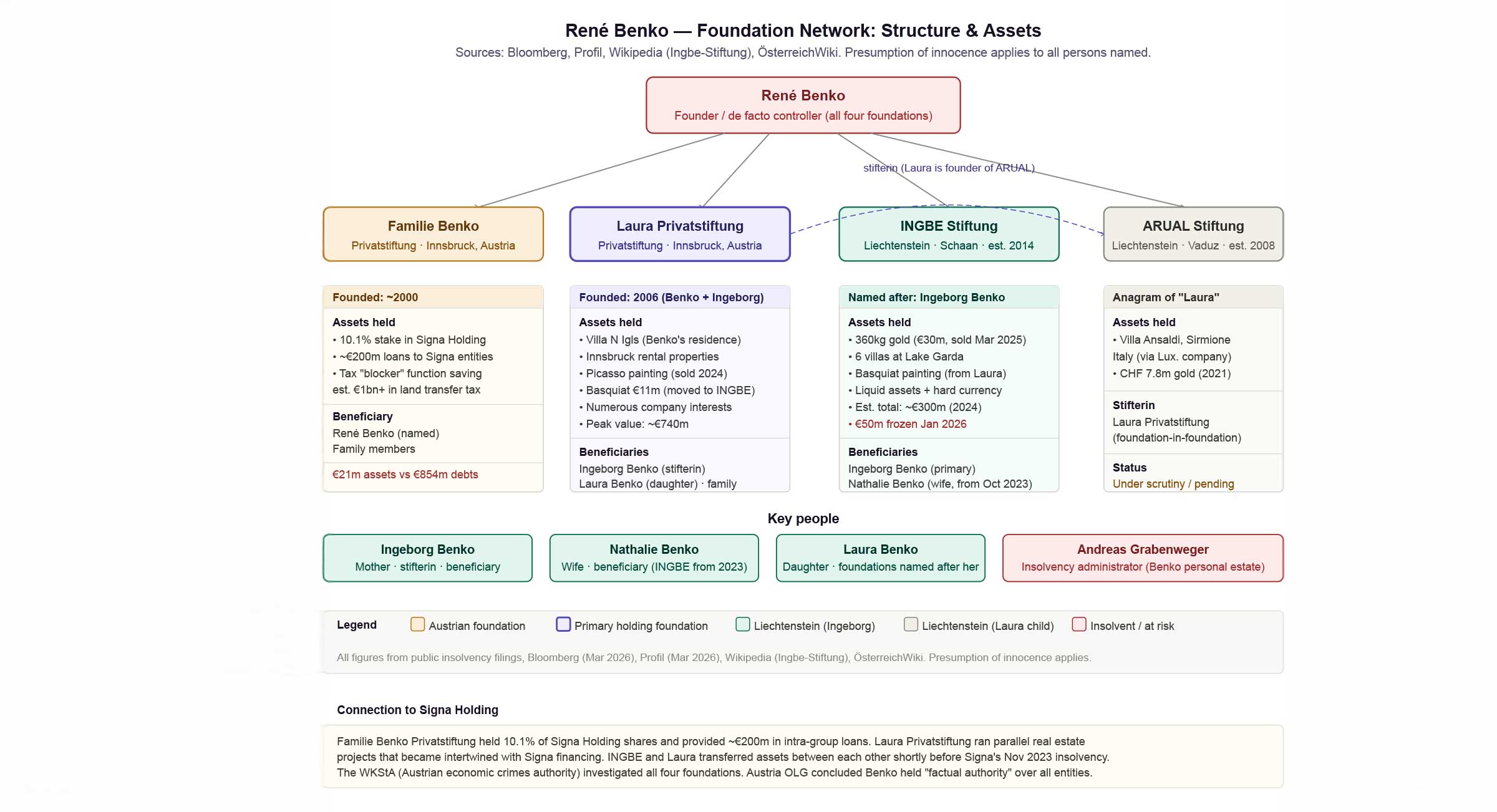

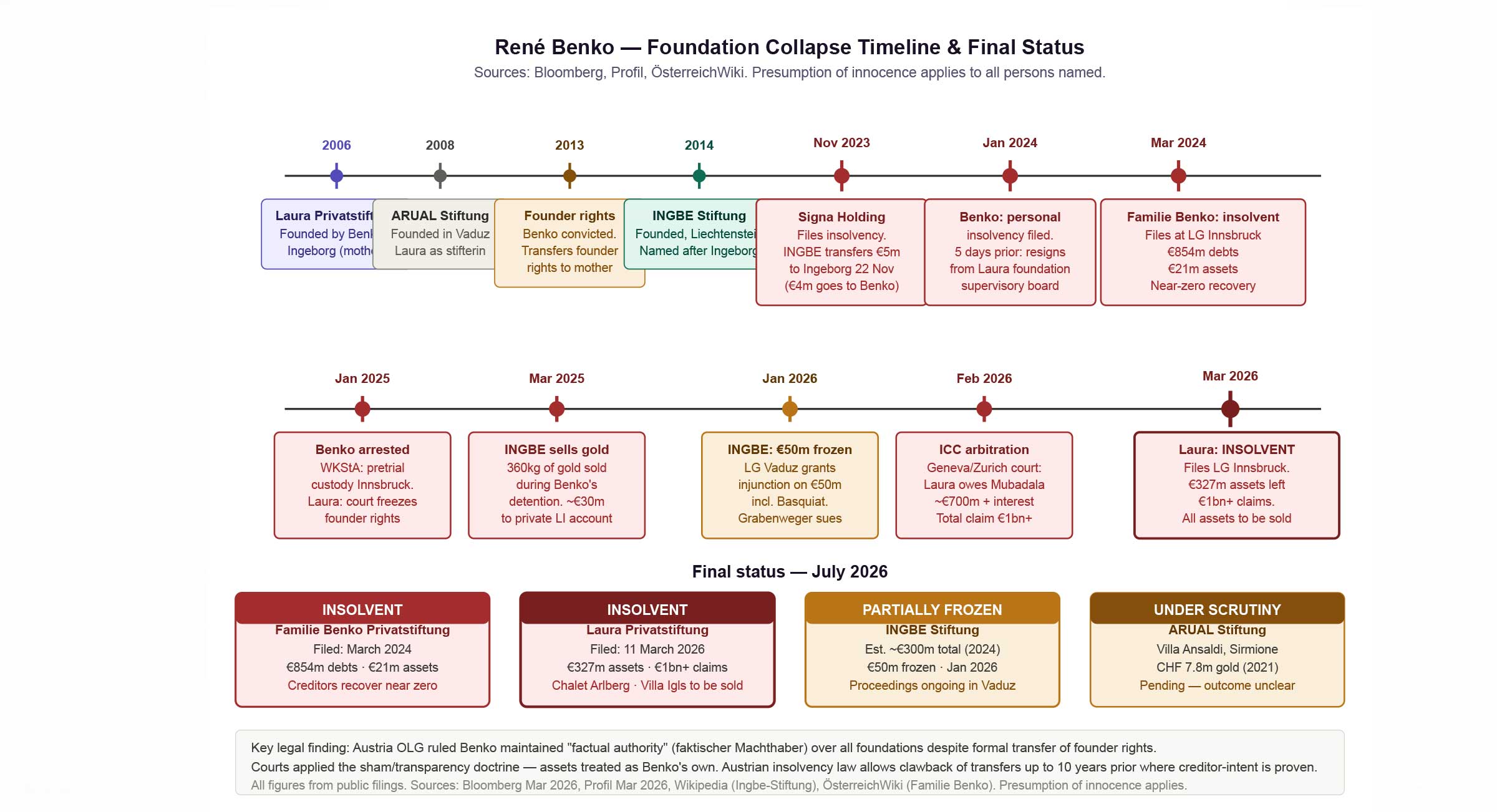

Benko distributed his private wealth across four foundations. Two were Austrian: the Familie Benko Privatstiftung and the Laura Privatstiftung, named after his daughter. Two were in Liechtenstein, including the INGBE Stiftung. The Laura Privatstiftung was the largest, holding primarily real estate with a reported market value of around 740 million euros at its peak. The Innsbruck villa where Benko continued to live in luxury even after filing for personal insolvency was not registered in his name. It belonged to the foundation. His wife Natalie and his daughter Laura were named as beneficiaries. Benko himself was reported to have stepped down as a beneficiary but continued to receive financial support through his mother, who was named as the stifterin, the person with founder rights, having taken over those rights from him in 2013 following a criminal conviction. Five days before filing for personal insolvency in January 2024, Benko resigned from the supervisory board of the foundation.

The four-foundation network built by René Benko: Familie Benko Privatstiftung (Austria), Laura Privatstiftung (Austria), INGBE Stiftung (Liechtenstein) and ARUAL Stiftung (Liechtenstein). Assets, beneficiaries, founding dates and cross-ownership connections. Sources: Bloomberg, Profil, Wikipedia (Ingbe-Stiftung), ÖsterreichWiki. Presumption of innocence applies.

Resigning from a foundation's supervisory board five days before filing for personal insolvency is not the act of someone exiting a structure with no further interest in it. It is the kind of last-minute manoeuvre that insolvency administrators and courts specifically look for when examining whether an alleged transfer of control was genuine. Under Austrian law — and under the laws of most EU member states — asset transfers to a foundation can be challenged by an insolvency administrator up to ten years after the transfer if the foundation was aware that the transfer was made with the intent to disadvantage creditors. The five-day gap did not help Benko's case.

Why the Foundations Failed

Several distinct legal mechanisms combined to defeat the asset protection that the Stiftung structure was intended to provide. They are worth understanding individually, because each one reflects a structural weakness inherent to European civil law foundations that offshore structures specifically address.

First: the insolvency clawback rules. Under Austrian insolvency law, asset transfers to a foundation can be challenged and reversed if they were made within the contestation period and if the debtor was insolvent at the time of transfer, or if the transfer was made without fair consideration (a gift), or if the foundation had knowledge that the transfer was intended to disadvantage creditors. The contestation period for gift-type transfers in Austria is two years before insolvency. In Germany it is four years. The German insolvency administrator used comparable provisions to reach into assets that Benko had transferred to the foundations. Under Austrian law, asset transfers when establishing the foundation and in the case of additional endowments are contestable if the transfer took place within ten years prior to the filing of the insolvency application and the foundation was aware at the time of the donation that the intention was to disadvantage creditors.

Second: retained control makes the structure transparent. Austrian courts applied what is called the transparency or sham doctrine to Benko's foundations. If the founder maintains effective control over a foundation — through a supervisory role, through the ability to influence distributions, or through continuing to benefit from the foundation's assets — the courts treat the foundation as an extension of the founder and the assets as if they still belong to him. Benko's continued residence in the foundation's villa, his continued receipt of funds through his mother as an intermediary, and his formal supervisory board membership (until five days before insolvency) all supported the argument that he had never genuinely relinquished control. It must be carefully examined whether the foundation is merely being used as a shell or an extension of the debtor and whether the debtor still exercises de facto control over the foundation. If so, certain legal transactions within the foundation could also be contested by the insolvency administrator.

Third: the Liechtenstein foundation came under Austrian prosecutor reach. Even the Liechtenstein INGBE Stiftung, which sits outside Austrian law, did not escape scrutiny. Austrian prosecutors confirmed that on 11 March 2025, during Benko's detention, the INGBE Stiftung in Liechtenstein sold more than 360 kilograms of gold valued at around 30 million euros, with the proceeds transferred to a private bank account in Liechtenstein. Austrian prosecutors used this as evidence of continued beneficial control and concealment of assets — exactly the kind of conduct that removes any credibility a foundation structure might otherwise have had as a genuine separation of assets. The Liechtenstein foundation, despite being outside Austria, was subject to the scrutiny of a major European mutual legal assistance process because Liechtenstein is a member of the European Economic Area and cooperates with EU judicial authorities.

Fourth: the Laura Privatstiftung filed its own insolvency. In March 2026 the Laura Privatstiftung filed for insolvency in Innsbruck after a court ruled it owed the Abu Dhabi sovereign wealth fund Mubadala Investment Company approximately one billion euros on soured investments. The assets that Benko had transferred into the foundation to protect them from his personal creditors had themselves generated new liabilities that the foundation could not meet. The 740 million euro real estate portfolio was now pledged, encumbered, and subject to an insolvency process of its own. His daughter's foundation, named in her honour and intended to provide for her, filed for bankruptcy. His wife and daughter were not immune from the consequences of a structure built with European foundations as its protective layer.

The complete collapse timeline: from the founding of Laura Privatstiftung in 2006 through the chain of insolvencies ending with the Laura foundation's own bankruptcy in March 2026. Final status of all four foundations shown at bottom. Sources: Bloomberg, Profil, ÖsterreichWiki. Presumption of innocence applies.

What Would Have Been Different With Offshore Structures

The question you raise is a legitimate and important one for anyone planning a wealth structure: if Benko had placed his assets in properly structured offshore foundations or trusts — in Nevis, the Cook Islands, or the Cayman Islands — would the outcome have been different?

The honest answer is: probably yes, at least in part. Not because offshore structures are invulnerable, but because they are specifically designed to address the weaknesses that defeated Benko's European foundations.

A Nevis trust, for example, is governed by Nevis trust legislation that places extremely strict limitations on creditor challenges: the challenge period is two years from the date of transfer, the creditor must prove fraudulent intent to the standard of beyond reasonable doubt (not the civil standard of balance of probabilities), and Nevis courts do not enforce foreign judgments as a matter of course. An Austrian or German insolvency administrator would need to commence entirely new legal proceedings in Nevis under Nevis law to reach those assets. That is expensive, slow, uncertain, and in many cases impractical.

A Cook Islands trust offers comparable protections. The Cook Islands International Trusts Act has never been successfully defeated by a foreign creditor in its decades of operation, which is why it remains the benchmark jurisdiction for asset protection trusts globally.

But here is the critical point, and it applies as much to offshore structures as it does to European ones: the protection only works if the structure was genuine and was established well before the problem arose. If Benko had established a Nevis trust in 2005, transferred assets into it genuinely and irrevocably, and had maintained no de facto control over those assets — no continued occupation of foundation properties, no informal distributions through family members, no supervisory board role — then the protections of an offshore trust would have been considerably more robust than what Austrian law provided.

In December 2025 Benko was found guilty of a second set of insolvency fraud charges, this time for hiding luxury watches from creditors. The Benko case is not primarily a story about the failure of foundations as a concept. It is a story about what happens when someone uses a foundation as a vehicle for concealment rather than genuine separation, when control is retained in substance while being relinquished on paper, and when the structure is built in a jurisdiction whose courts are subject to EU-wide mutual legal assistance and insolvency cooperation frameworks. European foundations exist within a tightly integrated legal area. Offshore structures exist outside it. That distinction, when it matters, matters enormously.

René Benko's case involved allegations of fraud and deliberate concealment that go well beyond the scope of ordinary asset protection planning. No legitimate offshore structure protects assets derived from fraud. What the case does illustrate clearly, for anyone with entirely legitimate assets and legitimate planning goals, is this: a European Stiftung provides legal separation in name but is subject to EU insolvency cooperation, civil law courts with broad reach, and contestation periods of up to ten years. An offshore trust or foundation in a properly chosen jurisdiction, established genuinely and well in advance of any foreseeable problem, provides structural protection that European law cannot easily penetrate. The choice of jurisdiction and the genuineness of the separation are not administrative details. They are the entire substance of the protection. 1Stop Connect and its accredited program partner help clients understand exactly what genuine separation looks like and which jurisdictions provide the framework to make it real.

What a Holding Company Does and Where It Falls Short

A holding company provides clean separation between operating entities and their assets. It does not, on its own, remove those assets from the shareholder's personal estate. That step requires a trust or foundation above it in the structure.

A holding company is a company incorporated under standard corporate law whose primary purpose is to hold interests in other companies, investment assets, real estate, or other property. It does not trade. It does not operate. It holds. Its main advantage is the legal separation it creates between the assets it holds and the operating companies below it: if an operating subsidiary runs into legal trouble, the assets held at the group level are not automatically exposed to that subsidiary's creditors.

Common offshore holding company jurisdictions include the British Virgin Islands, the Cayman Islands, Seychelles, Nevis, and Luxembourg within the EU. Within the UAE, the RAK International Corporate Centre (RAK ICC) and the Jebel Ali Free Zone (JAFZA) are popular holding vehicle jurisdictions, with DIFC and ADGM structures available for those requiring regulated environments. 1Stop Connect and its accredited program partner structures and administers holding companies across all of these jurisdictions as part of our international holding and trust services.

Where the holding company falls short as a standalone asset protection measure is straightforward: the shares of the company remain personal property of the shareholder. If the goal is to issue invoices, sign contracts, hold trading relationships, or act as a group holding company, the IBC is usually the most practical answer. That does not mean an IBC is always the right answer. If the commercial activity is secondary to a wider family wealth or asset protection plan, a Foundation or Trust may sit above the IBC, or hold the assets that matter most, while the company handles operations.

This is the key architectural principle that most clients grasp once it is explained but rarely arrive knowing: the company protects the assets inside it from the liabilities of the entities below it. But the company shares themselves remain in the shareholder's estate. To protect the company shares you need a trust or foundation above the company in the structure. The company and the trust or foundation are not alternatives. They are different layers of a complete structure.

Side by Side: The Full Comparison

| Feature | Trust | Foundation | Holding Company |

|---|---|---|---|

| Legal nature | Relationship, not an entity | Independent legal entity | Corporate entity |

| Who owns the assets | Trustee (legal); beneficiaries (beneficial) | The Foundation itself | The Company; shares owned by shareholder |

| Control by founder | Low in irrevocable trust — trustee decides | Medium — founder may hold reserved powers | High — shareholder controls the company |

| Creditor protection | Strongest — assets not in your estate | Strong — assets belong to the foundation | Limited — shares remain personal assets |

| Privacy | Very high — private deed, no public register | Charter public; regulations private | Shareholders often on public register |

| Banking | Trustee opens accounts as trustee | Foundation opens its own accounts | Company opens its own accounts |

| Succession | Excellent — assets bypass probate | Excellent — continues beyond founder's life | Shares pass through estate (probate) |

| Best for common law countries | Yes | Yes (increasingly) | Yes |

| Best for civil law countries | Risk of non-recognition | Yes — widely recognised | Yes |

| Setup complexity | Medium — trust deed, trustee appointment | Higher — charter, regulations, council | Low — standard incorporation |

| Annual maintenance | Trustee fees, compliance, accounting | Council fees, compliance, audit where required | Annual filing, accounting, registered agent |

| Key jurisdictions | Nevis, Cook Islands, DIFC, BVI, Cayman | Liechtenstein, Panama, Seychelles, DIFC, ADGM | BVI, Seychelles, Nevis, DIFC, RAK ICC, Luxembourg |

Asset Protection Against Creditors — Which Wins

If the primary goal is protecting assets from creditors, lawsuits, divorce proceedings, or forced heirship claims, the ranking is clear: an irrevocable discretionary trust structured well in advance of any dispute provides the strongest protection. The reason is simple. A trust's protection stems from the moment assets leave the settlor's ownership. Once transferred, they sit with the trustee, not the individual, placing them beyond the easy reach of creditors, litigants, or former spouses. Courts generally struggle to access assets that a person does not legally own. Discretionary trusts strengthen this barrier. Beneficiaries have no guaranteed entitlement, which means courts cannot simply assign or seize a distribution that may never occur.

Foundations provide strong protection through the same fundamental principle: once transferred, assets belong to the foundation and not to the founder. However, because foundations have a more visible legal presence (their charter is a public document and they must be registered with an authority), there is slightly more exposure compared to a well-structured private trust. That said, foundations are often superior for holding high-risk assets or operating companies because they own property in their own name, eliminating the complexities of split ownership inherent in trusts.

The timing of the transfer matters enormously for both structures. Most jurisdictions that provide strong asset protection legislation also have fraudulent transfer or fraudulent conveyance rules that allow courts to undo transfers made after a legal claim has arisen or when the transferor was already insolvent. The Nevis trust legislation specifically limits the period within which a creditor can challenge a transfer to two years, and places the burden of proof on the creditor at a high standard. This is one of the reasons Nevis remains a globally preferred jurisdiction for asset protection trusts. The lesson is consistent: structure before you need it, not after.

Control: The Most Misunderstood Trade-Off

The more control you retain over a trust or foundation, the less protection it provides. Courts in most jurisdictions will look past a structure where the founder or settlor maintains effective control and treat the assets as if they still belong to that person. This is called the "sham trust" doctrine and it has been applied by courts in the UK, Australia, the US and increasingly in the UAE context. Genuine protection requires genuine separation. The structures that protect the most are the ones where control has genuinely been relinquished — and that is the most difficult psychological shift for most clients to make.

This is the hardest conversation in asset protection planning and it is one I have repeatedly with clients over the years. People want to protect their assets without giving up control over them. The desire is completely understandable. But the law is not flexible on this point. If you maintain too much control over a trust or foundation, a court will look through the structure and treat the assets as yours. The protection disappears at exactly the moment it is needed most.

The foundation structure offers a middle path that many clients find more comfortable than a trust, precisely because the founder can retain certain defined rights through what are called reserved powers, without those powers being sufficient to constitute effective control. A DIFC Foundation blends features of both a company and a trust. It can have a Founder, Council Members, and Guardian, allowing family members or advisors to participate in governance. The Founder can retain influence via reserved powers or oversight mechanisms. A Trust, by contrast, is governed solely by Trustees, who owe fiduciary duties to beneficiaries, meaning the Settlor relinquishes control upon settlement.

A holding company gives you the most control of the three structures, but provides the least protection precisely because that control is indistinguishable from ownership in the eyes of the law. There is no structural distance between you and the assets.

Civil Law vs Common Law — Why Jurisdiction Matters More Than You Think

The legal system of the country where you live, where your assets are located, and where your beneficiaries will receive distributions can fundamentally change which structure makes sense for you. Trusts are preferred for those who live or operate in a common law country such as the UK, US, or offshore jurisdictions, and who want flexibility in changing beneficiaries or distribution terms. Foundations are preferred for those who have assets across multiple countries especially in civil law or mixed jurisdictions like the UAE, Liechtenstein, or Switzerland.

The specific risk with using a trust when you live in or hold assets in a civil law country is that the concept of split beneficial and legal ownership does not exist in those legal systems. A French court, a German court, or an Italian court may simply refuse to recognise the trust arrangement and treat the assets as though they still belong to the settlor. This risk is particularly acute for inheritance: forced heirship rules in civil law countries give certain family members an inviolable right to a share of the estate, and a foreign trust arrangement may not be sufficient to override those rights under local law. A foundation, which operates as a legal entity recognised under corporate principles that civil law courts understand, avoids this problem in most cases.

The UAE Context: DIFC, ADGM and Offshore Options

For clients based in or connected to the UAE, the structure options are particularly favourable. The UAE has zero personal income tax, zero capital gains tax, and zero inheritance tax. Assets held within a trust or foundation with UAE-based beneficiaries who are UAE tax residents are therefore not subject to any UAE-level taxation on distributions. This is an exceptional baseline from which to build a structure. Both options allow asset protection, inheritance planning, and tax efficiency when set up correctly under UAE or free zone regulations like ADGM or DIFC.

The DIFC Trust Law and the DIFC Foundation Regulations are both well-developed and internationally recognised. The DIFC Courts are a common law court with English as its working language, and their judgments are enforceable across most GCC countries and recognised in major international jurisdictions. ADGM operates an equivalent framework in Abu Dhabi with equally strong legal underpinning.

For clients who need more cost-effective offshore options or who want structures in jurisdictions outside the UAE, 1Stop Connect and its accredited program partner structures trusts and foundations in Nevis and Seychelles, both jurisdictions where we operate directly. Nevis is particularly well-regarded for trust structures. Seychelles is excellent for both foundations and holding companies. Both offer strong asset protection legislation, minimal filing requirements, and very competitive administration costs compared to DIFC or ADGM.

When You Need All Three — The Layered Structure

The complete asset protection architecture typically has three layers: a trust or foundation at the top, a holding company in the middle, and operating entities or investment assets below. Each layer serves a distinct purpose.

The most effective asset protection architecture for a business-owning family with cross-border assets typically uses all three structures in combination, each serving a specific purpose in the overall design.

At the top of the structure sits a trust or a foundation. This is the protective layer. It holds the shares of the company or companies below it. Assets at this level belong to the trustee (in a trust) or to the foundation itself, not to the founder or settlor. This layer provides the succession planning, the creditor protection, and the intergenerational continuity.

In the middle sits a holding company. This is the operational layer. It holds shares in operating subsidiaries, investment portfolios, real estate, and other asset classes. Operating activity, banking relationships, and contractual obligations live at this level or below it. The holding company provides clean separation between the operating world and the protective layer above it.

At the bottom sit operating companies, real estate vehicles, investment structures, or other purpose-specific entities. These carry the day-to-day commercial risk. If one fails or attracts a creditor, the loss is contained at that level and cannot easily propagate upward through the holding company into the protective structure above.

This layered approach is what 1Stop Connect's holdings and trusts service is built to design and implement. The right combination of jurisdictions, the right choice between trust and foundation at the top, the right holding company jurisdiction in the middle, and the right operating entity structure at the base depends entirely on the client's specific situation: where they live, where their assets are located, where their beneficiaries are based, and what their primary goals are.

"The most expensive asset protection structure is always the one you try to put in place after the problem has already arrived. The second most expensive is the one you chose without understanding what you were actually building."

— Dr. Dieter Hovorka, PhDFrequently Asked Questions

What is the main difference between a Trust and a Foundation? +

A trust is a relationship, not a legal entity. The settlor transfers assets to a trustee who holds them for beneficiaries under a trust deed. Legal ownership sits with the trustee. A foundation is a legal entity in its own right. It owns its assets independently, is governed by a council under a charter, and has its own separate legal personality. The core distinction: a trust is a relationship between parties; a foundation is an autonomous legal vehicle. For advice on which suits your specific situation, speak with 1Stop Connect and its accredited program partner.

Which structure offers the strongest asset protection against creditors? +

An irrevocable discretionary trust established well in advance of any dispute generally offers the strongest immediate creditor protection, because the assets legally belong to the trustee and beneficiaries have no guaranteed entitlement that courts can seize. Jurisdictions such as Nevis and the Cook Islands add additional statutory protection that places strict time limits and burden of proof requirements on any creditor challenge. Foundations also provide strong protection, but their formal legal personality is slightly more visible. A holding company alone provides the least protection, as shares remain personal assets of the shareholder.

Which is better for civil law country residents — Trust or Foundation? +

Foundations are generally the better choice for residents of civil law countries. The concept of split beneficial and legal ownership that underlies a trust does not exist in civil law systems, meaning local courts may refuse to recognise or may recharacterise trust arrangements. Foundations have their own legal personality and are more easily understood in civil law environments. Liechtenstein, Seychelles, Nevis, Panama, and the UAE's DIFC and ADGM all have well-developed foundation legislation.

Can I use a company instead of a Trust or Foundation for asset protection? +

A company can be part of an asset protection structure but rarely replaces a trust or foundation on its own. The shares of the company remain part of the shareholder's personal estate, accessible to creditors and subject to inheritance proceedings. Trusts and foundations sit above the company in the structure precisely to protect those shares. The company and the trust or foundation are not alternatives — they are different layers of a complete structure.

Is the UAE a good jurisdiction for setting up a Trust or Foundation? +

Yes, particularly through DIFC and ADGM, both of which have their own common law frameworks, independent courts, and dedicated trust and foundation legislation. The UAE has zero personal income tax, capital gains tax, and inheritance tax. DIFC Foundations and DIFC Trusts are internationally recognised structures used by families across the GCC, Asia, and Europe. Offshore options in Nevis and Seychelles, where 1Stop Connect operates directly, are also excellent and more cost-effective for many client profiles.

How do I know which structure is right for me? +

The right structure depends on where you live, where your assets are located, where your beneficiaries are based, what your primary goals are (creditor protection, succession, tax efficiency, privacy), and what legal system governs your home country. There is no universal answer. What there is, is a process of matching your specific situation to the available structures. 1Stop Connect and its accredited program partner provides this analysis as part of the initial consultation, at no charge and with no obligation.