The Middle East has transformed into a global business powerhouse over the past two decades, attracting entrepreneurs, multinational corporations, and investors from every corner of the world. The Gulf Cooperation Council states, particularly the United Arab Emirates, Bahrain, Qatar, and Saudi Arabia, have positioned themselves as premier destinations for international business establishment and regional headquarters.

As an accomplished founder and chairman bringing over a decade of leadership in international relations and diplomacy, I have witnessed firsthand how these four nations have evolved their business environments to compete on the global stage. My experience as a professor enhances my ability to mentor and guide emerging leaders while contributing to policy discussions that shape international affairs. My focus remains on innovative solutions that enhance understanding across cultures and foster global partnerships that drive economic growth and sustainable development in the region.

— Dr.Rashid Alameri

Understanding which Middle East hub suits your business objectives requires examining multiple factors that extend far beyond simple tax rates or company formation costs. Political stability, economic diversification efforts, market size, regulatory frameworks, and long term strategic vision all play crucial roles in determining where you should establish your presence in this dynamic region.

Let me guide you through a comprehensive analysis of these four major business hubs, drawing on my extensive experience in international relations and deep understanding of regional dynamics.

- United Arab Emirates: The Established Leader

- Bahrain: The Financial Services Specialist

- Qatar: The Strategic Investor

- Saudi Arabia: The Emerging Giant

- Tax Comparison Across the Four Hubs

- Oil Dependency and Economic Diversification

- Tourism and Economic Opening

- Offshore Jurisdictions in the Middle East

- How to Choose Your Middle East Hub

United Arab Emirates: The Established Leader

The United Arab Emirates stands as the most established and mature business hub in the Middle East, offering a combination of world class infrastructure, strategic geographic positioning, and business friendly regulations that few other locations worldwide can match.

With a federation of seven emirates, the UAE provides entrepreneurs with multiple options depending on their specific business needs and industry focus. Dubai and Abu Dhabi dominate as the primary commercial centers, while Sharjah, Ajman, and Ras Al Khaimah offer cost effective alternatives with their own unique advantages.

Dubai: The Global Trading Hub

Dubai has transformed itself from a modest trading port into one of the world's premier business destinations over just five decades. The emirate hosts over forty free zones, each catering to specific industries ranging from technology and media to logistics and healthcare.

The Dubai International Financial Centre operates as an onshore financial free zone with its own independent regulatory framework and common law legal system. This unique setup attracts international financial institutions, asset managers, and fintech companies seeking a regulated environment that aligns with global standards while providing access to Middle Eastern and African markets.

Dubai Multi Commodities Centre is another flagship free zone specializing in commodities trading, with over twenty thousand registered companies engaging in gold, diamonds, tea, and other commodity sectors. The DMCC provides a complete ecosystem including offices, warehousing, and direct access to Jebel Ali Port, the largest container port between Europe and Asia.

Beyond free zones, Dubai mainland company formation allows entrepreneurs to conduct business directly with the local UAE market and government entities without restrictions. Recent regulatory changes now permit one hundred percent foreign ownership in many mainland business activities, eliminating the previous requirement for a local UAE partner to hold fifty one percent equity in most sectors.

Abu Dhabi: The Capital's Growing Influence

Abu Dhabi, the UAE capital, has accelerated its business development initiatives through the Abu Dhabi Global Market, a financial free zone modeled on leading international financial centers. ADGM offers a robust regulatory framework based on English common law and attracts international banks, insurance companies, and professional service firms.

The emirate's sovereign wealth funds, including the Abu Dhabi Investment Authority managing assets exceeding one trillion USD, provide a stable financial foundation that reassures international investors about the long term viability of the market. Abu Dhabi's focus on sustainable industries, renewable energy, and advanced technology creates opportunities for businesses aligned with these strategic sectors.

Northern Emirates: Cost Effective Alternatives

Sharjah and Ras Al Khaimah present more affordable options for businesses that do not require the premium positioning of Dubai or Abu Dhabi. Sharjah Airport International Free Zone caters to logistics and trading companies, while RAK offers both onshore and offshore company formation options through RAK International Corporate Centre, providing confidential offshore structures recognized globally.

UAE Tax Environment

The UAE implemented a federal corporate tax effective from June 2023, marking a significant shift in its tax landscape. However, the rates remain highly competitive by global standards. Free zone companies meeting substance requirements pay zero percent corporate tax on qualifying income. Mainland companies and free zone entities not meeting requirements pay nine percent on taxable income exceeding 375,000 AED (approximately 102,000 USD).

No personal income tax exists in the UAE, making it attractive for entrepreneurs and executives. The five percent Value Added Tax introduced in 2018 applies to most goods and services, with exemptions for certain sectors including healthcare and education.

Withholding tax does not apply to most payments, and no capital gains tax or dividend tax burdens shareholders, creating a favorable environment for profitable enterprises and investment holding structures.

Economic Fundamentals

The UAE economy reached approximately 507 billion USD in GDP during 2025, making it the second largest economy in the Middle East after Saudi Arabia. Crucially, oil and gas now contribute only around thirty percent of GDP, demonstrating successful diversification into tourism, real estate, financial services, logistics, and technology sectors.

Dubai welcomed over twenty million international visitors in 2025, cementing its position as a global tourism and business events destination. The legacy infrastructure from Expo 2020 Dubai continues to drive business activity and innovation in the emirate.

For trading companies: Strategic location between Europe and Asia with world class logistics infrastructure.

For technology startups: Growing venture capital ecosystem, government support programs, and access to regional markets.

For holding companies: Zero tax on qualifying free zone income, extensive double taxation treaty network, and political stability.

For service businesses: Large expatriate market, strong consumer spending, and sophisticated business environment.

Bahrain: The Financial Services Specialist

The Kingdom of Bahrain has carved out a specialized niche as the Gulf region's premier financial services hub, leveraging its early mover advantage in banking and Islamic finance to build a sophisticated regulatory ecosystem that attracts international financial institutions.

Despite being the smallest GCC economy with a GDP of approximately 44 billion USD in 2025, Bahrain punches above its weight through strategic positioning and regulatory excellence. The kingdom's approach emphasizes quality over quantity, focusing on attracting the right types of businesses rather than simply maximizing company registrations.

Banking and Financial Services Excellence

Bahrain hosts the regional headquarters of numerous international banks, with the banking sector contributing significantly to GDP. The Central Bank of Bahrain maintains rigorous oversight while remaining pragmatic and business friendly in its approach to regulation.

The kingdom pioneered Islamic banking in the region and continues to lead in Shariah compliant financial services innovation. Islamic banks, takaful providers, and Islamic investment funds find Bahrain's regulatory framework particularly well suited to their needs, with clear guidelines developed over decades of practical experience.

Fintech companies increasingly view Bahrain as an attractive base due to the Central Bank's regulatory sandbox program, which allows innovative financial technology firms to test products in a controlled environment before full licensing. This progressive approach positions Bahrain ahead of regional competitors in embracing financial technology disruption.

Strategic Access to Saudi Market

The King Fahd Causeway connecting Bahrain to Saudi Arabia's Eastern Province provides a crucial competitive advantage. Businesses based in Bahrain can access the Saudi market while benefiting from Bahrain's more flexible regulatory environment and lower operating costs. Many companies use Bahrain as a regional base while conducting substantial business across the causeway in Saudi Arabia's much larger market.

This geographic proximity combined with cultural similarities and historical trading relationships makes Bahrain an ideal platform for companies seeking to serve the Saudi market without immediately committing to establishing operations within the kingdom itself.

Tax and Regulatory Environment

Bahrain maintains a zero percent corporate tax regime for most business activities, with taxation applying only to oil and gas companies and banks. This creates an extremely favorable environment for trading, services, and holding companies.

The kingdom implemented a five percent VAT in 2019, aligned with other GCC states. No personal income tax exists, and no withholding taxes apply to dividends, interest, or royalties in most circumstances, making Bahrain attractive for international corporate structures.

Company formation in Bahrain proceeds relatively quickly, with most business licenses issued within seven to fourteen days. The kingdom allows one hundred percent foreign ownership in most sectors without requiring a local partner, and recent regulatory reforms have simplified procedures further.

Economic Challenges and Opportunities

Bahrain faces economic challenges related to its small domestic market and limited natural resources compared to its Gulf neighbors. Oil and gas contribute only around eighteen percent of GDP, the lowest dependency in the GCC, reflecting successful diversification primarily into financial services.

The kingdom's close relationship with Saudi Arabia provides economic support and stability. Saudi financial assistance has helped Bahrain manage fiscal pressures, ensuring continued political and economic stability despite challenging regional conditions.

Real estate costs in Bahrain remain significantly lower than Dubai or Abu Dhabi, making it attractive for businesses seeking to minimize overheads while maintaining a Gulf presence. The more modest lifestyle costs also appeal to expatriate employees, potentially reducing employment expenses for companies.

Financial institutions: Comprehensive financial services licensing framework and Islamic banking expertise.

Fintech companies: Progressive regulatory sandbox and supportive Central Bank approach.

Saudi market entry: Physical access via causeway combined with easier operating environment.

Cost conscious businesses: Lower costs than UAE while maintaining Gulf presence and reputation.

Qatar: The Strategic Investor

The State of Qatar presents a unique business proposition centered around energy wealth, sovereign investment capabilities, and strategic independence in regional affairs. With a GDP of approximately 236 billion USD in 2025 and a small citizen population, Qatar enjoys one of the world's highest per capita income levels.

Qatar's business environment differs markedly from the more commercially driven approaches of the UAE and Bahrain. The state maintains tighter control over economic activity while selectively opening sectors to foreign participation when aligned with national development goals.

Qatar Financial Centre and Business Infrastructure

The Qatar Financial Centre operates as an onshore financial and business free zone in Doha, providing an independent legal and regulatory framework based on English common law. QFC attracts international firms seeking a regulated environment with protections familiar to Western businesses.

QFC companies benefit from zero percent corporate tax, full repatriation of profits and capital, and one hundred percent foreign ownership. The regulatory authority maintains high standards while remaining pragmatic in working with international businesses.

Recent reforms allow one hundred percent foreign ownership in many sectors outside the QFC as well, eliminating previous partnership requirements and opening additional opportunities for international investors in the broader Qatari economy.

Energy Sector Dominance

Qatar possesses the third largest natural gas reserves globally and stands as the world's leading exporter of liquefied natural gas. This energy wealth provides the foundation for Qatar's economic strength and sovereign investment activities through the Qatar Investment Authority, managing assets exceeding 450 billion USD.

Companies involved in energy services, engineering, and related sectors find substantial opportunities in Qatar's continued LNG expansion projects and energy infrastructure development. The state's focus on maintaining and growing its energy export capabilities creates ongoing demand for specialized services and expertise.

Post FIFA World Cup 2022 Infrastructure

Qatar's hosting of the FIFA World Cup 2022 accelerated infrastructure development, creating world class facilities for sports, hospitality, and events. The legacy infrastructure including stadiums, hotels, transportation networks, and the new Lusail City provides a foundation for diversifying beyond energy into tourism, business events, and sports management.

The tournament demonstrated Qatar's capability to deliver complex megaprojects and established the country as a viable destination for international events and tourism, albeit on a more modest scale than traditional tourism hubs like Dubai.

Tax and Operating Environment

Qatar applies a ten percent corporate tax rate on profits for most businesses, which remains competitive regionally though higher than Bahrain or UAE free zones. QFC entities enjoy complete tax exemption, creating an attractive option for qualifying activities.

No personal income tax exists in Qatar, and the country has not yet implemented VAT, providing a tax environment even more favorable than GCC neighbors in some respects. No withholding tax applies to dividends, interest, or royalties in most cases.

Company formation timelines in Qatar range from fourteen to thirty days depending on the business type and sector. The process involves more bureaucracy than UAE or Bahrain, reflecting Qatar's more measured approach to foreign business entry.

Strategic Considerations

Qatar maintains an independent foreign policy that sometimes diverges from other GCC states, most notably during the 2017 to 2021 diplomatic dispute with Saudi Arabia, UAE, Bahrain, and Egypt. While that crisis has been resolved, it demonstrated Qatar's willingness to pursue its own strategic interests even when facing regional pressure.

This independence can be viewed as either a strength or concern depending on perspective. Qatar's good relations with various global powers and regional actors, including maintaining ties with both Iran and Western nations, provides unique diplomatic access but also creates some geopolitical complexity.

Energy sector companies: Direct access to LNG projects and energy infrastructure development opportunities.

Large contractors: Government infrastructure projects and ongoing development of industrial zones.

QIA connected businesses: Companies seeking Qatar Investment Authority partnerships or contracts.

Sports and events: Leveraging World Cup legacy infrastructure for regional events and sports management.

Saudi Arabia: The Emerging Giant

The Kingdom of Saudi Arabia represents the largest and most ambitious transformation story in the Middle East through its comprehensive Vision 2030 economic diversification program. With a GDP exceeding 1.1 trillion USD in 2025, Saudi Arabia dwarfs other GCC economies in absolute size and offers a domestic market of over thirty five million people.

Understanding Saudi Arabia's business environment requires appreciating the magnitude and pace of change underway. Regulations, procedures, and opportunities that exist today may evolve rapidly as the kingdom pursues its ambitious transformation agenda under Crown Prince Mohammed bin Salman's leadership.

Vision 2030 Transformation

Vision 2030 encompasses hundreds of initiatives aimed at diversifying the Saudi economy away from oil dependency, developing new industries, attracting foreign investment, and creating employment opportunities for Saudi citizens. The program's scope extends far beyond typical economic development plans, touching virtually every aspect of Saudi society and economy.

Massive giga projects including NEOM, a planned 500 billion USD smart city in the northwest, The Red Sea luxury tourism development, and Qiddiya entertainment city near Riyadh demonstrate the kingdom's willingness to commit enormous resources toward economic transformation. These megaprojects create substantial opportunities for international companies across construction, engineering, technology, hospitality, and numerous other sectors.

The Public Investment Fund, Saudi Arabia's sovereign wealth fund, manages assets exceeding 700 billion USD and actively invests in strategic sectors both domestically and internationally. PIF's involvement signals priority areas for the kingdom's development and often creates partnership opportunities for international businesses.

Regulatory Reform and Foreign Investment

Saudi Arabia has undertaken significant regulatory reforms to attract foreign investment and improve ease of doing business. Recent changes allow one hundred percent foreign ownership in many previously restricted sectors, eliminating partnership requirements that historically deterred international investors.

The Saudi Arabian General Investment Authority now called Ministry of Investment of Saudi Arabia provides a one stop shop for investment licensing and facilitates entry for priority sectors and significant investors. The process has streamlined considerably compared to historical bureaucracy, though challenges remain for smaller businesses or less strategic sectors.

Special economic zones including King Abdullah Economic City and various industrial cities offer incentives including reduced land costs, streamlined approvals, and sector specific support for qualifying industries.

Market Size and Demographics

Saudi Arabia's large population, over sixty percent under thirty years old, creates substantial domestic demand across consumer goods, retail, healthcare, education, entertainment, and digital services. The kingdom's high smartphone penetration and growing e-commerce adoption present opportunities for technology enabled businesses.

Government initiatives to increase female workforce participation and expand women's economic role open new market segments previously underserved. Companies addressing these emerging needs through culturally appropriate products and services find receptive markets.

The concentration of wealth in Saudi Arabia, combined with a historically underdeveloped retail and service sector compared to the UAE, creates opportunities for international brands and service providers to establish dominant positions in a growing market.

Tax Environment

Saudi Arabia applies a twenty percent corporate tax rate on profits earned by foreign invested companies, higher than other GCC states but still competitive globally. The kingdom also imposes Zakat, an Islamic tax on Saudi and GCC national shareholders calculated at 2.5 percent of the Zakat base.

Withholding taxes apply to certain payments to non-residents, and VAT at five percent took effect in 2018, later increased to fifteen percent in 2020 during fiscal pressures. This remains the highest VAT rate in the GCC and represents a meaningful cost consideration for consumer facing businesses.

Tax incentives exist for priority sectors and investments aligned with Vision 2030 goals, potentially reducing effective tax rates for qualifying activities. The government continues developing these incentive programs to attract targeted foreign investment.

Cultural and Social Considerations

Saudi Arabia's conservative Islamic culture requires international businesses to adapt their operations and marketing approaches accordingly. Recent social reforms including allowing entertainment venues, cinemas, and mixed gender events expand business possibilities while still requiring cultural sensitivity.

Arabic language requirements for certain business documentation and government interactions present practical challenges for international companies. Local expertise becomes crucial for navigating cultural expectations and business customs.

The Saudization employment program requires companies to employ minimum percentages of Saudi nationals in their workforce, with quotas varying by sector and company size. Meeting these requirements while maintaining productivity and cost efficiency requires careful planning and execution.

Manufacturing and industry: Large domestic market, government support, and regional export base.

Healthcare and education: Growing private sector demand and government initiatives to expand capacity.

Technology and digital services: Young population, high smartphone adoption, and government digitalization push.

Tourism and hospitality: Ambitious expansion from 17 million to 100 million visitors by 2030.

Warning: Higher execution risk due to rapid change, cultural factors, and Saudization requirements.

Tax Comparison Across the Four Hubs

Understanding tax implications across Middle East jurisdictions proves crucial for structuring your business efficiently and managing long term costs effectively. While all four hubs offer favorable tax environments compared to Western Europe or North America, meaningful differences exist that impact specific business models differently.

Corporate Income Tax Rates

UAE applies zero percent corporate tax to free zone companies meeting substance requirements, and nine percent to mainland companies and non-qualifying free zone entities on income exceeding 375,000 AED. Bahrain maintains zero percent for most sectors except banking and oil. Qatar charges ten percent standard rate with QFC exemption. Saudi Arabia imposes twenty percent on foreign invested companies.

These headline rates tell only part of the story. Exemptions, incentives, and substance requirements significantly affect effective tax rates in practice. A UAE free zone company must demonstrate genuine economic activity including adequate employees, expenditure, and physical presence to qualify for zero percent treatment. Failure to meet substance tests results in the nine percent rate applying retroactively.

Personal Income Tax

No personal income tax exists in any of the four jurisdictions. This creates substantial advantages for entrepreneurs, executives, and employees who would face high marginal rates in their home countries. The absence of personal tax makes these hubs particularly attractive for wealth accumulation and personal financial planning.

Value Added Tax

UAE, Saudi Arabia, and Bahrain implemented five percent VAT, with Saudi increasing to fifteen percent in 2020. Qatar has not yet introduced VAT but plans remain for eventual implementation at an undetermined rate. For consumer businesses, these differences in VAT rates impact pricing competitiveness and profit margins.

Withholding Taxes

UAE generally does not impose withholding tax on dividends, interest, royalties, or service fees. Bahrain similarly avoids withholding taxes for most payment types. Qatar and Saudi Arabia may apply withholding taxes on certain payments to non-residents, particularly for royalties and technical fees, though double taxation treaties often reduce or eliminate these.

Tax Treaty Networks

UAE maintains an extensive network of over one hundred double taxation avoidance agreements, the most comprehensive in the region. This network provides significant advantages for international trading and holding structures. Bahrain and Qatar possess smaller treaty networks, while Saudi Arabia's network focuses on major trading partners and includes unique provisions for Zakat in treaties with Muslim majority countries.

Accessing treaty benefits requires demonstrating substance in the jurisdiction and proper documentation of tax residency. Simply incorporating a company without genuine activity will not provide treaty access under modern anti-avoidance rules.

Choose your jurisdiction based on business substance first, tax optimization second. Authorities globally scrutinize structures designed primarily for tax avoidance without commercial rationale. Ensure your structure reflects genuine business activity, decision making, and value creation in the chosen jurisdiction.

Consult qualified tax advisors in both the Middle East hub and your home country to understand the complete tax picture including CFC rules, transfer pricing, and substance requirements.

Oil Dependency and Economic Diversification

The Gulf region's historical dependence on oil and gas revenues has driven all four jurisdictions to pursue economic diversification with varying degrees of success and urgency. Understanding each hub's oil dependency and diversification progress provides insight into economic resilience and future trajectory.

Bahrain: Most Successfully Diversified

Bahrain stands out as the most successfully diversified Gulf economy with oil and gas contributing only around eighteen percent of GDP. The kingdom achieved this through decades of developing its financial services sector, establishing itself as the regional banking hub long before other Gulf states seriously pursued diversification.

This diversification was driven by necessity rather than choice, as Bahrain's oil reserves remain modest compared to neighbors. The kingdom processes Saudi oil at its refinery but lacks the petroleum wealth that allowed other Gulf states to delay diversification efforts.

The predominance of financial services, manufacturing, and tourism in Bahrain's economic mix provides resilience against oil price fluctuations. However, indirect dependency persists through Bahrain's close economic ties to Saudi Arabia and the financial support received from wealthier Gulf neighbors.

UAE: Successful Transformation

The UAE has reduced oil's contribution to approximately thirty percent of GDP, representing one of the most successful large scale diversification efforts globally. Dubai led this transformation, developing tourism, real estate, logistics, and financial services to the point where oil contributes only around five percent of the emirate's GDP.

Abu Dhabi, possessing the bulk of UAE oil reserves, maintains higher oil dependency around forty percent of emirate GDP. However, even Abu Dhabi actively diversifies through investments in renewable energy, technology, aerospace, and other sectors.

The UAE's diversification success provides economic stability and positions the country well for a post-petroleum future. Tourism alone now contributes over ten percent of GDP, while trade and logistics leverage geographic positioning to generate substantial revenues.

Saudi Arabia: Transformation Underway

Saudi Arabia faces the greatest diversification challenge due to the sheer scale of its economy and historical near total dependence on oil revenues. Despite progress, oil and gas still contribute approximately forty two percent of GDP and over sixty percent of government revenues.

Vision 2030 directly addresses this dependency through massive investments in tourism, entertainment, manufacturing, mining, and technology sectors. The commitment of hundreds of billions of dollars to megaprojects demonstrates seriousness about transformation.

The non-oil sector now exceeds half of GDP for the first time, representing meaningful progress. However, achieving the targeted reduction to fifteen percent oil dependency by 2030 requires sustained effort and successful execution of numerous initiatives.

Saudi Arabia's large population creates both challenge and opportunity for diversification. The need to employ millions of young Saudis provides urgency, while the domestic market size offers scale for new industries that smaller Gulf states cannot support.

Qatar: Wealthy but Dependent

Qatar's oil and gas sector contributes approximately sixty percent of GDP, the highest dependency among the four hubs. The massive natural gas reserves and small population mean Qatar lacks the same urgency for diversification that pressures less wealthy neighbors.

The Qatar Investment Authority's global investment portfolio provides diversification at the sovereign level even if the domestic economy remains heavily hydrocarbon focused. The 450 billion USD plus in foreign assets generates returns that can support the economy even if energy revenues decline.

Efforts to develop tourism, financial services, education, and healthcare create alternative revenue streams, but these initiatives face challenges competing against Dubai's established position and Saudi Arabia's market size.

For businesses, these varying dependency levels influence each hub's long term stability and commitment to business friendly policies. More diversified economies demonstrate proven ability to adapt and create opportunities beyond traditional sectors.

Tourism and Economic Opening

Tourism sector development reflects each jurisdiction's openness to international visitors and commitment to economic diversification. The sector creates substantial business opportunities in hospitality, entertainment, retail, and related services.

UAE: The Regional Leader

The UAE, particularly Dubai, dominates regional tourism with over twenty million international visitors in 2025. Dubai positions itself as a global destination for both leisure tourism and business events, leveraging world class hotels, shopping, entertainment, and airline connectivity through Emirates and Etihad.

Abu Dhabi develops cultural tourism through investments including the Louvre Abu Dhabi and forthcoming Guggenheim, complementing Dubai's more commercial focus. The emirate targets affluent travelers seeking luxury and cultural experiences.

The successful tourism model creates substantial employment and entrepreneurial opportunities in hospitality, tour operations, restaurants, retail, and entertainment. The sector's maturity means high competition but also proven demand and sophisticated infrastructure.

Saudi Arabia: Ambitious Expansion

Saudi Arabia targets one hundred million tourist visits annually by 2030, up from approximately seventeen million in 2023. This represents one of the world's most ambitious tourism expansion programs, requiring massive infrastructure investment and cultural adaptation.

The kingdom has opened tourist visas to citizens from forty nine countries, ending decades of restriction except for religious pilgrimage. Developments including AlUla archaeological sites, Red Sea luxury resorts, and Diriyah Gate historical district aim to create world class destinations.

For businesses, Saudi tourism expansion creates enormous opportunities but also execution risk. Success depends on infrastructure completion, service quality development, and marketing effectiveness against established competitors. Early movers may secure advantageous positions, but challenges around alcohol restrictions and conservative culture require creative solutions.

Qatar: World Cup Legacy

Qatar welcomed 1.4 million visitors during the FIFA World Cup 2022, demonstrating capability to host major international events. Post-tournament, the kingdom targets four to six million annual visitors through business events, sports tournaments, and cultural tourism.

The legacy infrastructure including Lusail City, world class stadiums, and expanded hotels provide the foundation for tourism growth. However, Qatar's small size and limited natural attractions create challenges competing against Dubai's established ecosystem or Saudi Arabia's scale.

Business opportunities in Qatar tourism focus on premium segments, business events leveraging the convention infrastructure, and sports related tourism building on World Cup success and ongoing sports event hosting.

Bahrain: Niche Tourism

Bahrain attracts approximately eleven million visitors annually, primarily from Saudi Arabia crossing the causeway for weekends and holidays. The kingdom serves as a more liberal escape for Saudi visitors seeking entertainment and dining options unavailable at home.

Cultural and historical tourism around Bahrain Fort, the pearling heritage sites, and motorsports through the Bahrain International Circuit provide niche attractions. The Formula One Grand Prix generates significant annual visitor activity.

Tourism business opportunities in Bahrain center on serving the Saudi weekend market and developing specialized niches rather than competing for global leisure tourism against better positioned neighbors.

Offshore Jurisdictions in the Middle East

Beyond traditional onshore business establishment, the Middle East offers several offshore jurisdiction options for holding companies, international trading structures, and asset protection vehicles. Understanding these offshore alternatives provides additional structuring flexibility for appropriate use cases.

RAK International Corporate Centre (UAE)

Ras Al Khaimah International Corporate Centre operates as a legitimate offshore jurisdiction within the UAE, providing confidential company structures with zero tax on all income. RAK ICC companies cannot conduct business within the UAE itself, focusing instead on international trading, holding, and consulting activities.

The jurisdiction maintains a register of beneficial owners confidentially, meeting international transparency standards while protecting privacy from public disclosure. RAK ICC has established credibility globally through proper regulation and compliance with FATF requirements.

Banking access for RAK offshore companies has become more challenging as international banks scrutinize offshore structures. However, reputable banks will work with properly documented structures serving legitimate business purposes with clear economic substance.

Jebel Ali Free Zone Offshore (UAE)

Jebel Ali Free Zone Authority offers offshore company licenses distinct from standard free zone companies. These offshore entities provide confidentiality and tax exemption similar to RAK ICC while carrying the JAFZA brand recognition.

Offshore companies from JAFZA serve similar purposes to RAK ICC, focusing on international activities outside UAE. The same banking and substance considerations apply, requiring clear business rationale and proper documentation for financial services access.

Qatar Financial Centre Offshore

QFC provides structuring options suitable for holding companies and international investment vehicles, though technically not a pure offshore regime. The regulatory framework allows for structures minimizing operational requirements while maintaining credibility with international financial institutions.

Entities established in QFC for holding purposes or fund management can benefit from zero tax and access to Qatar's treaty network where substance requirements are met. This positions QFC as an attractive alternative to traditional offshore locations for certain use cases.

Saudi Arabia and Bahrain Approaches

Saudi Arabia does not offer traditional offshore company formation. The kingdom focuses on attracting onshore investment and business establishment, with incentives and special zones providing benefits without offshore privacy structures.

Bahrain maintains offshore banking units for banks but does not offer traditional offshore company formation for general businesses. The kingdom's zero tax mainland regime for most activities reduces the need for separate offshore structures.

When to Consider Offshore

Offshore structures serve legitimate purposes including holding investments in multiple countries, managing international intellectual property, and consolidating family assets. However, they must be established and operated properly to provide intended benefits.

Modern international transparency standards including Common Reporting Standard and beneficial ownership registers mean offshore does not provide the tax opacity it once did. Home country tax authorities can access ownership information, making offshore primarily a structuring tool rather than tax avoidance vehicle.

Banks, payment processors, and business partners increasingly scrutinize offshore companies. Success requires clear documentation of business purpose, economic substance, and beneficial ownership. Pure shell companies with no substance face account closures and transaction restrictions.

Critical Requirements: Offshore companies must have genuine business purpose, documented substance, and transparent beneficial ownership to access banking and maintain credibility.

Do not use offshore to: Hide assets from legitimate authorities, evade taxes in your residence country, or conduct business without proper licensing.

Do use offshore when: Consolidating international holdings, managing multi-jurisdictional IP, or structuring international trading in tax efficient manner with proper substance.

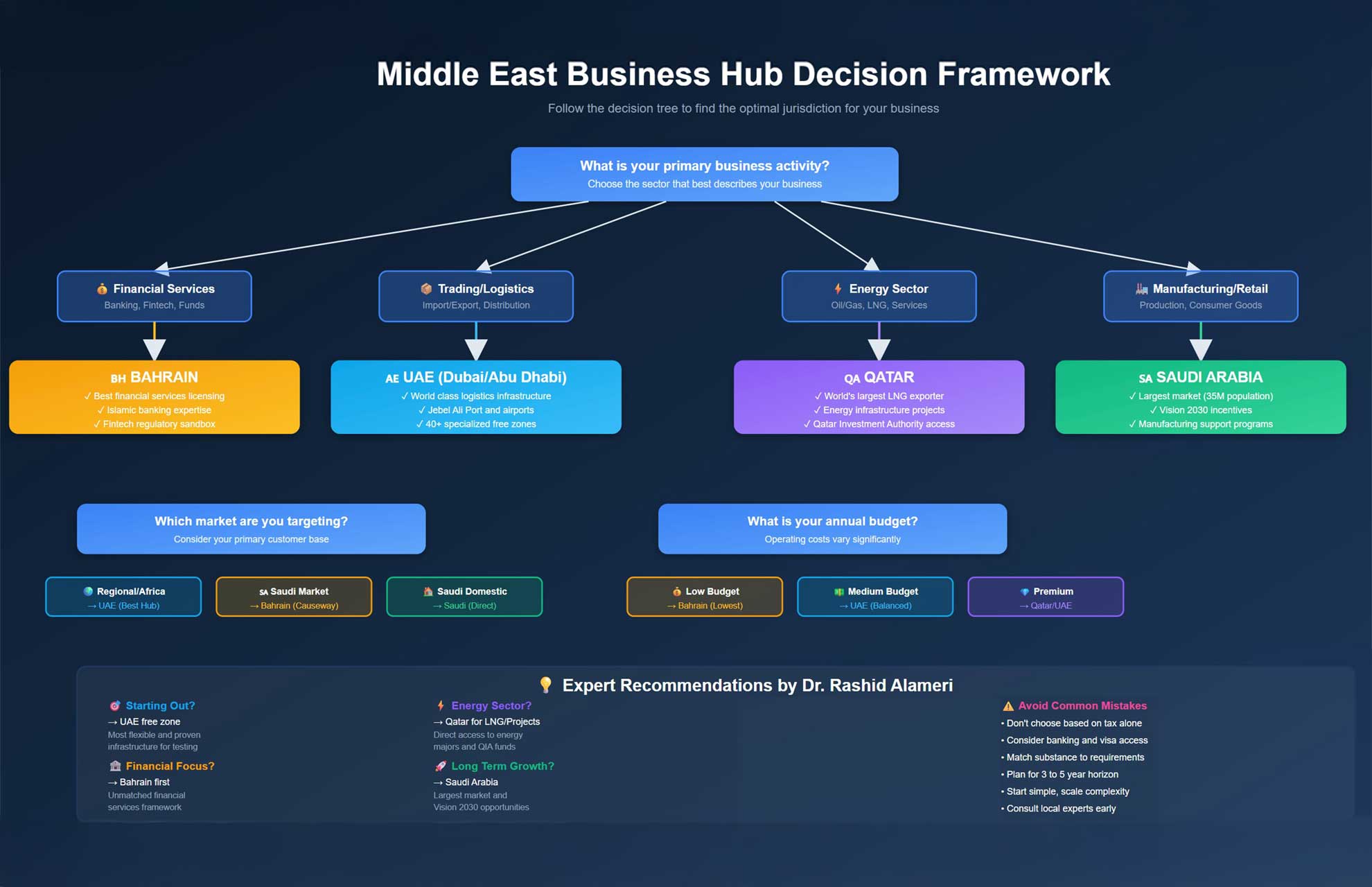

How to Choose Your Middle East Hub

Selecting the optimal Middle East jurisdiction for your business requires balancing multiple factors based on your specific circumstances, industry, growth plans, and strategic objectives. Let me provide a decision framework based on my experience guiding international businesses through this choice.

Step 1: Define Your Primary Business Activity

Your core business activity often determines the most suitable jurisdiction before considering other factors.

Financial services or fintech: Bahrain offers the most comprehensive financial regulatory framework and licensing options. Qatar Financial Centre works for larger institutions or fund managers. UAE DIFC or ADGM suit banks and asset managers seeking Gulf and African market access.

Trading and logistics: UAE dominates through Jebel Ali Port, airport infrastructure, and free zone options. Bahrain provides cost effective alternative for smaller traders. Saudi and Qatar offer limited advantages for pure trading operations.

Technology and startups: UAE leads in venture capital availability, startup ecosystem maturity, and talent availability. Saudi Arabia offers scale for technology addressing mass market needs. Bahrain and Qatar have smaller tech ecosystems.

Manufacturing and industry: Saudi Arabia provides domestic market size, government incentives, and regional export base. UAE offers logistics and access to materials. Bahrain and Qatar have limited manufacturing appeal.

Consulting and professional services: UAE provides the largest professional services market and regional project flow. Bahrain works for Saudi focused consultancies. Qatar suits energy and infrastructure specialists. Saudi opportunities exist but require local presence and partnerships.

Step 2: Assess Your Market Focus

Targeting UAE market: Establish in UAE either free zone or mainland depending on customer requirements and contract types.

Targeting Saudi market: Consider Bahrain for cautious entry maintaining flexibility, or establish in Saudi Arabia for serious market commitment and scale.

Regional Middle East and Africa: UAE provides the best infrastructure for serving multiple markets from a single hub.

Specific to Qatar or energy sector: Qatar establishment makes sense for energy focus or QIA related opportunities.

Global operations with Gulf presence: UAE free zone offers flexibility for international operations while maintaining Middle East footprint.

Step 3: Consider Your Growth Timeline

Testing the market: Start with UAE free zone offering low commitment and flexibility. Bahrain provides inexpensive entry if Saudi market potential exists.

Scaling proven business: Commit to jurisdiction matching primary market. Invest in mainland presence if targeting local customers and government.

Building for long term: Evaluate Saudi Arabia seriously despite challenges, given market size and transformation opportunities.

Step 4: Evaluate Practical Factors

Residence and lifestyle: UAE offers the most developed expatriate lifestyle, international schools, and cosmopolitan environment. Saudi Arabia is improving rapidly but remains more conservative. Bahrain and Qatar fall between UAE and Saudi.

Employee recruitment: UAE attracts talent most easily given reputation and lifestyle. Saudi Arabia faces challenges but offers large salary packages. Qatar and Bahrain have smaller talent pools.

Operating costs: Bahrain typically lowest for office and housing. UAE mid to high range. Qatar and Saudi Arabia comparable to UAE depending on city and sector.

Travel connectivity: UAE leads dramatically with Emirates and Etihad networks. Qatar Airways provides good connectivity from Doha. Saudi and Bahrain have improving but less extensive options.

Step 5: Plan for Complexity

Many successful regional businesses establish entities in multiple jurisdictions as they scale. Start simple with a single entity, prove the business model, then expand to additional markets when revenue and operations justify the complexity.

A common evolution involves starting in UAE to test the market, adding Bahrain or Saudi presence to pursue those markets, and potentially establishing offshore holding structures once the business reaches significant scale.

Most international businesses should start in the UAE unless their business model specifically requires another location. The UAE offers the most mature business environment, the easiest operational framework, and the greatest flexibility for regional expansion.

Consider Bahrain if you have specific Saudi market focus or financial services licensing needs. Evaluate Qatar if your business connects to energy sector or sovereign investment opportunities. Assess Saudi Arabia if targeting the kingdom's large market and willing to navigate transformation complexities.

Remember that initial jurisdiction choice does not lock you in permanently. Business structures can evolve as your company grows and opportunities emerge across the region.

This article provides educational information about Middle East as business hub for company structures based on regulations as of March 2026. It is not legal advice. It is not tax advice. It is not a substitute for professional consultation.

Company formation laws, tax regulations, and substance requirements change. What is accurate today may change tomorrow. Licensing requirements vary by country and specific business activity. Banking policies change frequently.

The information here is accurate to our knowledge as of publication but carries no warranty. Laws change. Regulations evolve. Always verify current requirements before proceeding.

If you would like to discuss your specific situation, contact us directly. That is exactly what we are here for.